Safaricom Sale: Finding the Right Mix for Growth, Ownership, and Fiscal Prudence

As Kenya enters a pivotal phase of its economic roadmap, the government’s plan to sell its sizeable stake in Safaricom —the country’s most valuable company and its telecoms leader—has ignited far-reaching debate and investor anticipation. Combining budgetary imperatives with inclusive ownership and strategic capital, the Safaricom divestment may set the pace for privatization across Africa’s frontier markets.

Thank you for reading this post, don't forget to subscribe!Why the Government Is Selling

Kenya’s Treasury is tasked with raising approximately KSh 149 billion by mid-2026. With limited big-ticket assets available, divesting from Safaricom emerges as the practical and impactful solution to plug a sizable fiscal deficit, reduce reliance on public debt, and finance the 2025/26 budget cycle. While other state firms—such as Kenya Pipeline Company—are in the mix, Safaricom’s market value, profitability, and iconic brand make it the anchor of Kenya’s privatization drive.

What’s on Offer and Who Wants It

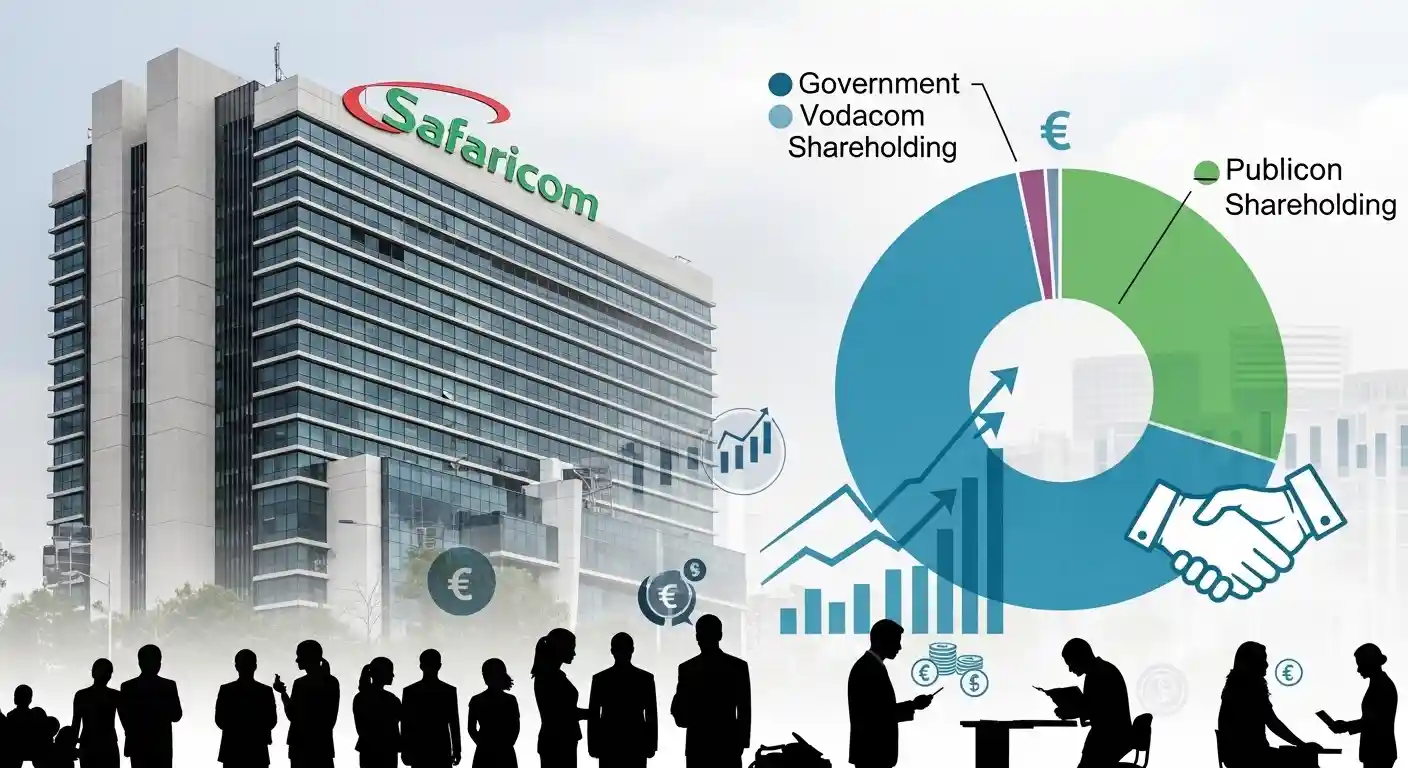

Currently, the government holds a 34.9% stake in Safaricom (worth about KSh 418 billion). Vodacom Group

, with a 39.9% holding, remains the largest shareholder. The rest—about 25.2%—is owned by public and other institutional investors. Interest from global telecom groups, private equity, and institutional funds is high, especially since Safaricom maintains strong cash flows from M‑Pesa, mobile data, and its new Ethiopian expansion.

Chart: Safaricom’s Shareholding Structure

Can Kenyan Investors Go It Alone?

While Kenyan retail and corporate investors have consistently shown enthusiasm—Safaricom’s initial 2008 IPO was oversubscribed fivefold—the market’s depth is not enough to absorb the government’s entire stake today. Pension funds, asset managers, and high-net-worth individuals could take up substantial allocations, but the sheer scale (KSh 280–418 billion) means local buyers would need strong external backing to avoid portfolio risk and liquidity crunches. Analysts, regulators, and Treasury officials agree: foreign capital is indispensable for a transaction of this magnitude, although broad local participation remains a political and economic priority.

A Workable Sale Structure: Mixing Public and Private Placement

To maximize value, ensure stability, and foster inclusion, an optimal mix for the Safaricom divestiture would look like this:

Block Sale to Strategic Investors

Sell a significant portion (10–20%) via a negotiated block deal to global telecom groups (such as Vodacom Group ), sovereign funds, or reputable private equity investors. Block sales offer price certainty, can attract a premium on market rates, and signal investor confidence.

Such deals are less disruptive to the market, safeguard Safaricom’s operational stability, and attract partners with long-term sectoral expertise.

Secondary Public Offering

Float the remaining shares (5–10%) via a public offer on the Nairobi Securities Exchange, aimed at retail and institutional Kenyan investors.

History shows major public offers build a culture of local ownership, stimulate wealth creation, and support market liquidity. Oversubscription is likely, so allocation rules must be robust to ensure fair distribution.

Benefits and Risks

This blended approach secures the government against selling cheaply in a thin market, spreads ownership, and anchors Safaricom firmly in Kenya’s social and economic fabric.

However, risks remain: concentrated block sales can lead to foreign dominance, and overambitious public offers could depress prices if local demand softens.

Safaricom’s Performance and Investor Sentiment

Safaricom recently reported a 52.1% rise in half-year profit to KSh 42.7 billion, buoyed by M-Pesa’s double-digit growth and reduced losses in its Ethiopian operation. Revenue from mobile financial services hit KSh 88.1 billion, as fixed internet and mobile data continue to outpace voice revenue in the firm’s business mix. With dividends rising and interim payouts scheduled, investor appetite shows no sign of weakening.

Policy, Socioeconomic Impact, and What Comes Next

A successful sale promises to fulfill fiscal needs, spark market innovation, and reinforce Kenya’s position as a frontier for international capital. For policymakers, the imperative is to avoid past mistakes—selling at undervalued prices, restricting access, or allowing single-buyer dominance. Clear rules and strong communication will be pivotal.

For citizens and corporates, participation offers the chance to own a piece of Kenya’s premier enterprise. For Safaricom itself, the transaction will likely open doors for stronger partnerships and new growth avenues, especially in mobile money and regional expansion.

Conclusion

The planned sale of the government’s stake in Safaricom blends financial necessity, strategic thinking, and social impact. Only a carefully managed mix—balancing block sales to strategic investors with open access for the Kenyan public—can maximize returns, deepen market engagement, and keep Kenya’s telecom crown jewel on a path of sustainable growth.